As the trucking industry gears up for a significant shift, the impending 25% tariff on heavy trucks, set to take effect on October 1, 2025, promises to stir considerable debate and controversy. Announced by former President Donald Trump, this bold move aims to protect U.S. manufacturers from the perceived threat posed by international competition, reinforcing the administration’s commitment to bolster domestic production in an era of global trade complexities.

However, the implications of this decision extend far beyond mere protectionism. Stakeholders are left grappling with questions about inflated costs, reduced competition, and potential backlash from trade partners, highlighting the precarious balance between safeguarding American jobs and fostering a robust market environment.

The announcement has already triggered a notable response in financial markets, with shares of companies like Paccar reportedly rising, indicating a mixed market sentiment surrounding this contentious policy. As industry experts and manufacturers prepare for this new reality, the looming tariff raises critical concerns about its long-term impact on pricing strategies, operational efficiencies, and the overall dynamics of the heavy truck market.

Will this be a boon for homegrown manufacturers, or could it inadvertently stifle innovation and competition?

Historical Context for Tariffs in the Trucking Industry

Tariffs have historically played a crucial role in shaping the dynamics of the U.S. trucking industry, influencing operational costs, trade volumes, and supply chain relationships. Analyzing significant tariff events provides insights into their impacts and the lessons learned that resonate with current tariff discussions.

1. The Chicken Tax (1964)

In response to European tariffs on U.S. poultry, the U.S. government implemented a 25% tariff on light trucks, known as the “Chicken Tax.” This protective measure led to a drastic decline in imports of certain vehicles, such as the Volkswagen Type 2, and effectively shielded domestic automakers from foreign competition in the light truck segment. Remarkably, this tariff remains in place today, continuing to influence market dynamics and the pricing strategies of light trucks in the U.S. [source]

2. Tariffs on Steel and Aluminum (2018)

The Trump administration’s tariffs on imported steel and aluminum significantly increased costs for U.S. truck manufacturers. Paccar, a leading producer in the field, projected an additional $75 million in costs attributed to these tariffs, prompting manufacturers to explore cost-saving measures. Many opted to source materials from Mexico to exploit duty-free provisions available under the US-Mexico-Canada Agreement (USMCA). This shift indicated a growing trend of adapting sourcing strategies in light of changing tariff landscapes [source].

3. Tariffs on Heavy-Duty Trucks (2025)

In September 2025, the U.S. announced a new 25% tariff on imports of heavy-duty trucks, effective from October 1. This announcement triggered immediate market reactions, resulting in declines in stock prices of major manufacturers such as Daimler Truck and Traton. Analysts estimated potential financial losses for Daimler at between €700 million to €800 million, although price adjustments were anticipated to mitigate some of the impact. This incident illustrates the volatile nature of tariffs and their immediate effects on stock markets and investment strategies [source].

Lessons Learned

- Supply Chain Vulnerabilities: Tariffs can disrupt established supply chains, leading to increased costs and operational challenges. Companies have recognized the importance of diversifying suppliers and considering regional manufacturing to navigate potential risks.

- Market Adaptation: The trucking industry has continuously adapted to shifting tariff landscapes through alternative sourcing strategies, pricing adjustments, and sometimes passing increased costs onto consumers.

- Policy Implications: Tariff policies can bear unintended consequences, such as market distortions and strained international trade relations. Both policymakers and industry stakeholders increasingly acknowledge the need for balanced approaches that protect domestic industries while maintaining healthy trade relationships.

Understanding the historical context surrounding tariffs in the trucking industry helps elucidate their significant impacts on industry dynamics and the potential implications of recent tariff announcements.

| Trucking Company | Market Position | Recent Financial Performance (Q3 2025) | Impact of 25% Tariff |

|---|---|---|---|

| Mack Trucks | Subsidiary of Volvo Group, known for its Class 8 trucks, high reputation for durability. | Operating profit: 13.5 billion SEK ($1.39 billion), reported a strong commitment to technology and connectivity. | Increased production costs due to tariffs, plans for local manufacturing to mitigate impact. |

| Volvo | Leading global manufacturer, strong in Europe and North America, focused on sustainability. | Q3 adjusted operating profit decreased by 17% to 11.7 billion SEK ($1.2 billion). | Tariffs expected to exacerbate ongoing market decline in North America. |

| Peterbilt | Division of PACCAR, strong market share in North America, known for innovation. | Net income of $590 million, market share combined with Kenworth at 30.4% in Q3 2025. | Beneficiary of tariffs but facing higher costs for inputs affected by tariffs on components. |

| Kenworth | Another division of PACCAR focusing on reliability and performance. | Revenue of $6.67 billion for Q3 2025, adjusted down from earlier forecasts. | Significant impact on production costs, pushing for more domestic production. |

| Freightliner | Dominant market share of 38.4% in Q1 2025, strong focus on technology. | Sales plummeted by nearly 40% to 30,225 units due to market pressures. | Positioned to leverage domestic production advantages, but cautious on future sales. |

Economic Implications of the 25% Tariff on Heavy Trucks

The new 25% tariff on heavy trucks will have broad economic effects. From rising costs to disrupted supply chains, understanding the ramifications is crucial.

Increased Costs for Trucking Companies

- The tariff will significantly raise the price of heavy-duty trucks.

- The American Trucking Associations (ATA) estimates that a new Class 8 truck could cost around $30,000 more.

- Small carriers with thin profit margins may struggle to expand their fleets or replace old vehicles.

- Companies might also have to find new financing options, which could increase their financial burden.

- Like previous automotive tariffs, these cost increases may affect raw material prices and operational expenses source.

Supply Chain Disruptions

- Tariffs can disrupt supply chains.

- Trucking companies that depend on imported parts might need to source from domestic suppliers, causing delays and possible production stoppages.

- Adjusting sourcing strategies could lead to higher transportation costs, which may affect the entire market source.

Impact on Freight Rates

- As operational costs rise, trucking companies might increase their freight rates.

- The competitive market could limit how much they can raise prices.

- Higher costs could tighten profit margins, especially for smaller carriers.

- If consumer prices rise due to tariffs, demand for freight services could also drop, leading to fewer shipments.

- This could create a ripple effect, impacting demand for goods and inflation rates source.

Lessons from Recent Tariff Scenarios

- Past tariffs in other sectors have shown significant economic impacts.

- The auto industry suffered $108 billion in costs linked to tariffs, forcing companies to reassess their supply chains source.

- Early indications from manufacturers like Daimler Truck highlight sharp declines in sales related to tariff changes source.

In conclusion, the economic effects of the 25% tariff on heavy trucks will impact costs, supply chains, and freight rates. Stakeholders must brace for these changes as they reshape the trucking industry’s dynamics.

Consumer Impact of the 25% Tariff on Heavy Trucks

The impending 25% tariff on heavy trucks is poised to significantly impact consumers, both directly and indirectly. This decision, while aimed at bolstering domestic manufacturers, raises serious concerns about rising prices, decreased supply chain efficiencies, and the overall economic landscape.

Increased Costs for Fleet Acquisition and Operation

With the tariff taking effect, the costs associated with purchasing heavy trucks are expected to surge. The American Trucking Association projects that the price of new Class 8 tractors could rise by approximately $30,000. Given the narrow profit margins typically seen in the trucking industry, these increased equipment costs may hinder fleet expansions and modernization plans among trucking companies, leading to a ripple effect felt by consumers. Smaller trucking companies, in particular, may struggle to cope with these inflated costs, potentially leading to decreased competition in the market.

Rise in Freight Service Prices

As trucking companies face escalating operational costs due to tariffs, many may feel compelled to pass these expenses onto shippers and end consumers. Such price hikes for freight services are already being observed in the form of increased spot rates on key cross-border routes, with some rising by as much as 30% to 40%. Given that freight costs are components of overall consumer prices, these increases could contribute to higher prices for goods and services, ultimately affecting consumer purchasing power and economic trends [source].

Supply Chain Disruptions

Tariffs disrupt established supply chains, leading to logistical inefficiencies. Many trucking companies may need to adjust their sourcing strategies, potentially moving towards more costly domestic suppliers to mitigate tariff impacts. This shift can create delays and uncertainty in delivery times, compounding challenges for businesses that rely on just-in-time manufacturing and distribution models. As a result, consumers may experience not only increased prices but also potential shortages in certain product categories [source].

Hesitance in Fleet Modernization

The rise in costs associated with purchasing new trucks could result in a notable hesitance among trucking companies to modernize their fleets. Many operators may delay vehicle replacements or seek alternative financing options, limiting the adoption of advanced, fuel-efficient trucks. This stagnation could ultimately affect the industry’s environmental performance and efficiency, as older, less efficient trucks remain on the road longer than anticipated. Industry experts have noted that continued reliance on outdated equipment could lead to higher operational inefficiencies and further cost increases that would be passed down to consumers [source].

Overall Economic Implications for Consumers

The overall economic implications of the 25% tariff on heavy trucks may manifest in broader inflationary pressures across various sectors. Increased freight and operational costs could erode consumer purchasing power, especially in a market already grappling with inflation. Historical data shows that similar tariffs previously enacted in the automotive sector led to significant financial repercussions, with manufacturers facing billions in additional costs—which were eventually passed on to consumers [source]. As the trucking industry begins to navigate these turbulent waters, stakeholders must remain vigilant regarding the potential ramifications for both consumers and the marketplace at large.

In summary, the consumer impact of the 25% tariff on heavy trucks will likely manifest in increased prices for freight services, disruptions in supply chain efficiency, and hesitance in needed fleet modernization. As these economic consequences continue to unfold, careful monitoring of the trucking industry’s response will be essential.

Perspectives on the 25% Tariff on Heavy Trucks

Donald Trump, Former President of the United States

“In order to protect our Great Heavy Truck Manufacturers from unfair outside competition, I will be imposing, as of October 1st, 2025, a 25% Tariff on all ‘Heavy (Big!) Trucks’ made in other parts of the World.”

This statement emphasizes the administration’s focus on shielding U.S. manufacturers from foreign competition, aiming to bolster domestic production within the heavy truck market.

“We need our Truckers to be financially healthy and strong, for many reasons, but above all else, for National Security purposes!”

Here, Trump connects the health of the trucking industry to national security, suggesting the importance of maintaining a robust domestic manufacturing base.

Chris Spear, President and CEO of the American Trucking Associations (ATA)

“A 25% tariff levied on Mexico could see the price of a new tractor increase by as much as $35,000. That is cost-prohibitive for many small carriers, and, for larger fleets, it would add tens of millions of dollars in annual operating costs.”

Spear highlights the financial strain that tariffs could impose on both small and large trucking companies, indicating that the ripple effects may lead to higher consumer costs for goods transported by truck.

Peter Voorhoeve, President of Volvo Trucks North America

“Volvo has implemented a $3,500 tariff surcharge on new trucks; however, this does not fully cover the additional costs incurred from tariffs on foreign-sourced components, steel, and aluminum.”

Voorhoeve describes the challenges faced by Volvo despite manufacturing in the U.S., pointing out that reliance on imported components leads to increased operational costs, showcasing an “unintended consequence” of U.S. tariff policies.

These quotes collectively underscore the varying perspectives within the trucking industry regarding the significant 25% tariff on heavy trucks, revealing a tension between protectionist policies intended to support domestic manufacturing and the consequential financial burdens placed on trucking companies and consumers alike.

Conclusion

In summary, the 25% tariff on heavy trucks set to take effect on October 1, 2025, presents a complex blend of challenges and opportunities for the trucking industry. As stakeholders navigate the repercussions of this significant policy, the immediate implications include increased costs for fleet acquisition, a potential tightening of profit margins, and disruptions to established supply chains. The projected price hike of approximately $30,000 for new Class 8 tractors could particularly strain smaller carriers already operating on thin margins, resulting in delayed fleet upgrades and modernization efforts.

On the other hand, this policy aims to bolster domestic manufacturers by insulating them from foreign competition, allowing for a potential increase in market share for U.S.-based companies. Companies like Paccar and Mack Trucks may benefit from a strengthened market position as imported trucks become less competitive due to higher costs. However, the effectiveness of this protectionist measure remains uncertain, given the likelihood of rising operational costs that may ultimately be passed on to consumers through higher freight rates.

Furthermore, while some domestic manufacturers may thrive, the broader economic landscape could face inflationary pressures as costs rise across the board. The historical context of tariffs indicates that the repercussions might resonate throughout the industry, just as previous tariff policies have done, leading to significant adjustments in market dynamics.

As the industry gears up for these changes, careful attention to the pricing strategies and supply chain modifications will be essential. Stakeholders must assess how this tariff will reshape the financial and operational landscape, balancing the need for protection of domestic jobs against the critical need for competition and innovation in the trucking sector. As the deadline approaches, the trucking community must prepare for a transformative period that could redefine its operational strategies and market interactions for years to come.

Electric Truck Adoption Data in the United States

As the electric vehicle (EV) market continues to evolve, the adoption of electric trucks in the U.S. is experiencing notable growth, although it still represents a small segment of the overall trucking industry. In 2024, over 1,700 electric trucks were sold, maintaining steady sales compared to 2023. This brought the cumulative total to more than 3,400 electric trucks sold in the U.S. up to the end of 2024. Key drivers for this increase include substantial government incentives, such as a tax credit of up to $40,000 for buyers of electric trucks, alongside funding opportunities through the nearly $1 billion Clean Heavy-Duty Vehicles Grant Program aimed at supporting vehicle purchases and the development of charging infrastructure (IEA).

Challenges Ahead

Despite these positive developments, the landscape for electric truck adoption in the U.S. is adjusting due to recent policy changes. In April 2025, a 25% tariff was imposed on imported automobiles and auto parts, which impacts all segments of the automotive industry, including electric trucks. Estimates indicate that this tariff could lead to an approximate $4,000 increase in production costs per vehicle for manufacturers like Tesla, effectively raising consumer prices by around 9% (Promwad).

Moreover, a newly proposed federal fee of $250 for electric vehicle owners is intended to generate additional funding for infrastructure but raises concerns about the overall cost burden on EV owners. This fee aligns poorly with the average federal gas tax paid by traditional vehicle owners, potentially deterring potential buyers from transitioning to electric options (Kiplinger).

Market Projections and Industry Response

In light of these tariffs and costs, analysts project a potential sales dip of 15% for electric trucks in the short term, resulting in job losses across associated sectors and dealerships (Promwad). Nonetheless, initiatives aimed at increasing the accessibility of electric trucks persist. For instance, Climate United has announced a $250 million investment plan to acquire up to 500 electric semi-trucks, which it will lease out at competitive rates to support operators at California ports (Reuters).

Conclusion

Overall, while the electric truck market in the United States is progressing with supportive policies aiding growth, the abrupt impact of tariffs and new fees could significantly influence adoption rates. It remains critical for stakeholders in the trucking industry to navigate these evolving challenges while promoting sustainable solutions and innovations to advance the transition towards electrification in their fleets.

Responses from Trucking Companies to the 25% Tariff

As the 25% tariff on imported heavy trucks looms, various trucking companies are recalibrating their strategies to adapt to a rapidly changing economic landscape. Companies like Paccar, Mack Trucks, and Daimler Truck are among those responding to this significant policy shift, each with unique impacts based on their market positions and operational structures.

Paccar Inc.

Paccar, which manufactures the popular Peterbilt and Kenworth brands, stands to benefit significantly from the new tariffs. The company currently produces over 90% of its trucks in the U.S., which strengthens its market position against competitors heavily reliant on imports. Following the tariff announcement, Paccar’s stock price surged, indicating investor confidence in the company’s ability to leverage the tariff to increase its market share in the domestic trucking industry. Analysts suggest that Paccar might consider further increasing production capacity in the U.S. to capitalize on the reduced competition from imported trucks [source].

Mack Trucks and Volvo Group

In contrast, Mack Trucks, owned by Volvo Group, has voiced significant concerns about the tariffs. The company announced workforce reductions, planning to lay off between 550 to 800 employees across its U.S. facilities. Such layoffs stem from anticipated demand declines attributed to freight rate uncertainties and rising truck prices due to tariffs. The uncertainty surrounding the tariffs has led Volvo to revise its forecasts for the North American truck market, expecting a long-term decline in demand as pricing pressures mount [source].

Daimler Truck

Daimler Truck, known for its Freightliner brand, has reported a nearly 40% decline in North American sales for Q3 2025, driven by market sentiment and the expected implications of the tariffs. Despite operating manufacturing plants in the U.S. and Mexico, Daimler grapples with the potential for increased costs due to components that could be affected by the tariffs. The company is likely to reassess its production strategies to mitigate risks and navigate the challenging post-tariff market landscape [source].

Industry-Wide Challenges

Overall, the American Trucking Associations (ATA) caution that the tariffs could raise purchase prices significantly, with estimates of an increase by up to $35,000 per tractor. This change exacerbates the financial strain on small and medium carriers, potentially reducing competition in the industry while further tightening profit margins. As many trucking companies confront heightened operational costs due to these tariffs, the ripple effects on pricing strategies and supply chain dynamics are expected to be profound [source].

In summary, while companies like Paccar aim to enhance their competitive edge through domestic production, brands like Mack Trucks and Daimler face a more uncertain future as they navigate potential job cuts, declining sales, and a rapidly evolving market affected by the new tariff landscape.

Selected Industry Insights:

- Paccar’s robust domestic production shields it from tariffs, likely enhancing its market position.

- Mack Trucks and Volvo are adjusting workforce and forecasting declines due to tariff impacts.

- Daimler Truck grapples with a sales downturn, reflecting broader market uncertainties and tariff consequences.

Each company’s approach to addressing the tariff policy will shape the future competitive dynamics within the trucking sector, as they strive to balance costs and maintain profit margins in a challenging economic environment.

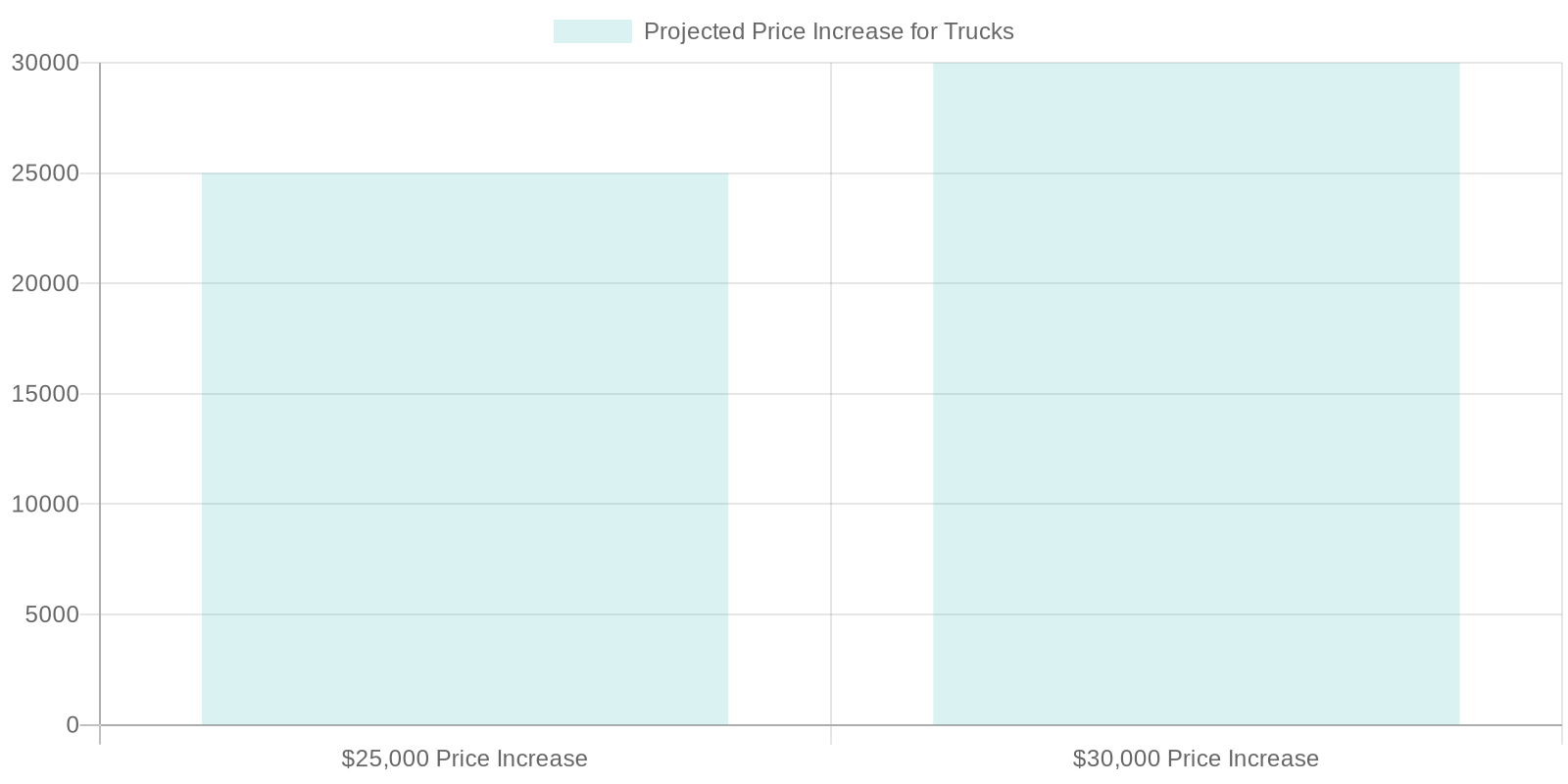

Key Images and Graphs on Tariff Impacts

Projected Price Increase Due to Tariffs

Graph showing anticipated price increases due to the 25% tariff on heavy trucks. The cost of procurement is expected to rise dramatically, affecting small and large trucking firms in the market.

Influence of Tariffs on Heavy Trucks

Image depicting heavy trucks at a border checkpoint, highlighting the effects of tariffs on international trade and trucking operations.

Infographic on Tariff Impacts

An infographic representing the various impacts of tariffs on the trucking industry, including cost increases and supply chain disruptions.

The combination of these visuals underscores the extensive ramifications that the 25% tariff on heavy trucks could impose on the industry.

Personal Stories and Testimonials from the Trucking Industry

As the 25% tariff on heavy trucks looms closer to implementation, industry stakeholders have shared insights that capture the emotional and operational turmoil caused by this new policy. Here are some personal stories and testimonials that showcase the impacts felt across the trucking landscape:

Chris Spear, President & CEO of the American Trucking Associations (ATA)

Spear emphasized the strain these tariffs could have on the industry, stating:

“A 25% tariff could see the price of a new tractor increase by as much as $35,000. That is cost-prohibitive for many small carriers and, for larger fleets, it would add tens of millions of dollars in annual operating costs. We are already seeing increased freight costs and reduced volumes as a direct result of these tariffs, causing significant anxiety among your average truck driver who relies on their job to support their families.”

Paccar Inc.

Reflections from Paccar executives reveal significant operational anxiety:

“We are looking at an estimated $75 million in additional costs in Q3 2025 alone, and we know that these costs may force us to make tough decisions. Some of our competitors who manufacture trucks outside the U.S. will have a competitive cost advantage that could hurt our market share. It’s a stressful time for everyone in the company and for the small businesses that depend on us for jobs and livelihoods.”

Truckload Carriers Association (TCA)

The TCA shared the sentiments of many small carriers, stating:

“Our members have already faced immense challenges due to rising costs. Any additional tariffs on imported truck parts or essential components would spell disaster for profitability and job security for drivers and employees. The freight industry is already operating in a difficult environment; these tariffs could be the tipping point for many carriers.”

A Small Carrier’s Perspective

John, an owner-operator based in Ohio, voiced his frustrations:

“As a small truck owner, every cent counts. With the upcoming tariff, we’re talking about price increases that might not only affect my ability to replace my aging truck but could also mean passing costs onto my clients. This means less work, and potentially I may have to let go of my trusted driver who’s been with me for years. This isn’t just a financial issue; it’s personal. My business, my job, and my employees’ futures are on the line.”

Industry Concerns from the Trucking Community

A reflection from the Saskatchewan Trucking Association:

“These tariffs threaten to devastate an industry already grappling with the worst freight economy in 40 years. We fear the loss of countless trucking jobs and operators who might just walk away due to prohibitive costs. These are not just industry statistics; they represent real families that depend on trucking for their livelihood.”

Each of these perspectives illustrates the emotional toll of the new tariff structure and the pressing concerns among industry players about the future viability of their businesses. The interdependence of trucking companies, their employees, and the broader economy becomes more evident as such policies unfold, reinforcing the urgent need for balanced approaches that support both domestic production and vital industry stakeholders.