The recent imposition of a 25% tariff on heavy trucks not made in the United States adds more complexity to an industry already facing many challenges. Former President Donald Trump announced these tariffs to protect domestic manufacturers by creating a barrier around the U.S. trucking sector. However, the implications extend well beyond protections for manufacturers; they threaten to raise trucking industry costs for fleet operators and, ultimately, result in higher prices for consumers.

Industry leaders, including the American Trucking Associations, have expressed concern about the heavy truck market impact caused by retaliation from international trading partners and rising costs in the trucking industry. As companies like Peterbilt and Freightliner prepare for these challenges, a key question remains: can the benefits of these tariffs justify the financial strain on the broader industry? The stakes are high for an industry already dealing with rising operational costs.

The recent announcement of a 25% tariff on heavy trucks not manufactured in the United States has drawn significant concern from industry stakeholders. President Donald Trump stated that this move is essential to protect domestic truck manufacturers from unfair foreign competition, referring to it as a necessary measure for national security. However, the implications of these tariffs extend far beyond intended protective measures.

Chris Spear, President of the American Trucking Associations (ATA), criticized the tariffs, noting, “at a time when the industry is just beginning to recover, these tariffs can decrease freight volumes and increase costs for motor carriers.” He warned that the financial burden on fleet operators could be substantial, with prices for new trucks expected to rise significantly—potentially by $35,000 per vehicle due to the tariffs. This escalation in costs comes at an inopportune moment when many operators are already facing financial strain.

Peter Voorhoeve, President of Volvo Trucks North America, while not directly quoted in the sources consulted, represents an industry that stands to be affected despite manufacturing trucks domestically. The rise in tariffs could prove challenging for Volvo and similar companies as they work to navigate a landscape plagued by increased operational costs and market volatility. Analysts have noted that although the tariffs may provide temporary benefits to companies like Paccar and Freightliner, the broader consequences might undermine truck availability and sustainability in the long-run.

Overall, the sentiment among industry leaders is critical, emphasizing that while shielding domestic production is crucial, the financial repercussions of such tariffs could jeopardize the recovery and stability of the trucking industry. Many stakeholders fear that these tariffs might not only inflate truck prices but could also disrupt established supply chains, fundamentally altering the competitive landscape in a sector that is pivotal to the U.S. economy.

- The tariff rate on heavy trucks will increase from 0% to 25%, effective October 1, 2025.

- Following the announcement, Paccar saw a notable stock surge, with shares climbing 6% in pre-market trading.

- The American Trucking Associations formally opposed the tariffs, highlighting concerns about increased costs for truck buyers and potential market disruptions.

- Industry leaders warn that the tariffs could lead to significant price hikes for new trucks, estimated to add approximately $35,000 per vehicle.

- Critics, including Chris Spear of the ATA, emphasize that these tariffs may decrease freight volumes and impose financial strains on motor carriers already facing challenges.

- The backlash against the tariffs indicates possible retaliation from international trading partners, posing further risks to trade relations.

| Manufacturer | Market Share (%) | Key Features |

|---|---|---|

| Peterbilt | 22 | High-quality interior, customizable options, fuel efficiency |

| Freightliner | 25 | Aerodynamic design, advanced safety features, great resale value |

| Mack Trucks | 16 | Powerful engines, durable construction, driver comfort |

| Volvo | 12 | Innovative technology, eco-friendly options, smooth handling |

| Manufacturer | Market Share (%) | Key Features |

|---|---|---|

| Peterbilt | 22 | High-quality interior, customizable options, fuel efficiency |

| Freightliner | 25 | Aerodynamic design, advanced safety features, great resale value |

| Mack Trucks | 16 | Powerful engines, durable construction, driver comfort |

| Volvo | 12 | Innovative technology, eco-friendly options, smooth handling |

Potential Price Increases Due to 25% Tariffs

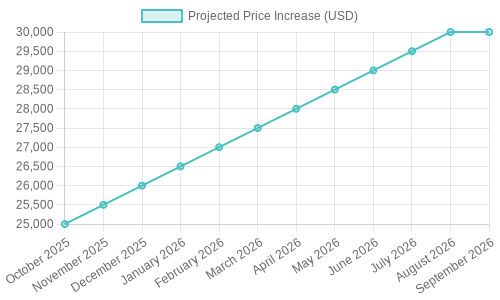

The recent implementation of a 25% tariff on heavy trucks imported into the United States is projected to have significant repercussions on pricing within the industry. Industry experts estimate that the average price of a heavy truck could increase by approximately $25,000 to $30,000. This is largely due to the added costs associated with tariffs that are now levied on imported vehicles and parts.

Implications for Manufacturers and Fleets

Manufacturers are already responding to the tariff situation by announcing price hikes for new vehicle models. As evident from multiple sources, companies such as Volvo Trucks North America and Mack Trucks are adjusting their pricing strategies to reflect the new costs. This adjustment is expected to take effect as early as May 2025, and with the rising prices, it raises concerns for fleet operators who depend heavily on imported trucks and components.

Domestic production, although ramping up, is unlikely to meet the current market demand for heavy trucks, as U.S. factories produce approximately 300,000 medium and heavy trucks annually, whereas the reliance on imported trucks remains high. Experts observe that the tariffs will force trucking companies either to absorb these increased costs or pass them onto consumers, leading to inflationary pressures across the sector.

Economic Impact

The broader economic implications are also significant. According to analysis from the Center for Automotive Research, these tariffs could ultimately cost U.S. automakers about $108 billion in 2025, including an estimated additional cost of nearly $5,000 per vehicle. This price increase could lead to a substantial decrease in consumer purchasing capacity and significantly lower vehicle sales in the market. Furthermore, trucking demand is predicted to decrease by about 17% if the tariffs persist into the end of this year, potentially negating earlier forecasts of market growth.

Operational Challenges

These developments indicate a precarious situation for trucking companies already navigating a challenging economic landscape shaped by rising operational costs. Many carriers are expressing concerns that these tariffs will exacerbate the ongoing freight recession, leading to tighter capital formation and potentially driving some smaller operators out of business due to insufficient margins.

In conclusion, the 25% tariffs are not just a protectionist measure but a catalyst for significant price hikes and operational challenges that threaten to disrupt the entire trucking industry. Industry leaders are advised to brace for a period of volatility as they adapt to these shifting dynamics in the market.

The implementation of a 25% tariff on heavy trucks not manufactured in the United States is fraught with implications that can significantly alter the landscape of the trucking industry. This policy, positioned as a necessary safeguard for domestic manufacturers, could very well escalate the operating costs for fleet operators who are already squeezed by a myriad of economic pressures. Industry leaders, including Chris Spear of the American Trucking Associations, have openly criticized this tariff as a detrimental force that threatens to inflate vehicle prices and undermine market stability. With projected price increases of $25,000 to $35,000 per truck, the strain on motor carriers could lead to reduced freight volumes and ultimately harm the economic recovery that the sector is attempting to navigate.

As domestic production attempts to ramp up in response to these tariffs, there are significant doubts about whether it can meet the robust demand for heavy trucks, given that U.S. factories have historically struggled to keep pace. Furthermore, international tensions loom, potentially resulting in retaliatory measures that could worsen trade relations, further complicating an already fragile economic environment. The trucking industry, a backbone of the U.S. economy, must brace itself for an era of unpredictability as these tariffs play out.

In essence, the fallout from the 25% tariff will likely extend well past the boundaries of economic strategy; it carries the risk of breeding inflation, threatening not only the survival of many trucking businesses but also the overall health of the economy. Key stakeholders in the trucking industry are urged to prepare for a tumultuous future as they navigate the repercussions of this stark shift in trade policy. It is evident that while the intent behind the tariffs might be as a protective measure, the consequences may be counterproductive, leading to an industry grappling with higher costs and reduced competitiveness on the global stage.

Historical Context of Tariffs on the Auto Industry and Heavy Trucks

The United States has a long history of implementing tariffs to protect domestic industries, including the automotive sector. A significant historical example is the Smoot-Hawley Tariff Act of 1930, which aimed to protect American manufacturers by imposing high tariffs on imported goods, including automobiles. This move led to international retaliation and a substantial decline in global trade, showcasing how such tariffs can negatively impact the economy.

Another notable instance is the “Chicken Tax” of 1964, which imposed a 25% tariff on light trucks in response to European tariffs on U.S. chicken exports. While this effectively shielded domestic truck manufacturers from foreign competition, it has resulted in a long-lasting distortion in the market, impacting pricing and standardization.

The recent 25% tariffs on heavy trucks, announced in October 2025, align with historical trends but come with unique challenges. Analysts estimate that these tariffs could increase costs for manufacturers, potentially adding between $2,000 and $12,000 per vehicle, varying by model. Furthermore, significant decreases in sales (up to 40% for some manufacturers) and stock price volatility were observed following the tariff announcement. Concerns about international retaliation and the disruption of trade relations are prevalent, similar to past instances of tariff implementations.

In summary, while tariffs have historically aimed to protect domestic industries, their consequences often include economic instability, market distortions, and challenges for both consumers and manufacturers. The historical context of such tariffs provides insights into the potential outcomes of the current situation concerning the heavy truck industry.

The historical examples of tariffs on the automotive sector highlight potential implications of the new 25% tariffs on heavy trucks. These past tariffs, notably the Smoot-Hawley Tariff and the Chicken Tax, resulted in varying degrees of trade retaliation and market distortion. The Smoot-Hawley Tariff led to significant international pushback that worsened the Great Depression by curtailing global trade and causing widespread economic hardship.

The Chicken Tax created a safety net for American light truck manufacturers, yet its long-term effect has been a lack of competition in the market, often leading to higher prices for consumers. Similar patterns are expected to occur with the 25% tariffs on heavy trucks, where manufacturers might raise prices by thousands of dollars per vehicle. Moreover, the projected decline in sales could mirror historical downturns caused by tariffs, creating an adverse cycle of increased costs and reduced consumer purchasing power. The potential for retaliatory measures from trading partners adds another layer of complexity and potential for economic fallout, reshaping future trade dynamics.

Industry Leader Quotes on 25% Tariffs on Heavy Trucks

The recent 25% tariff on heavy trucks imported into the United States, announced by President Donald Trump, has elicited sharp reactions from across the industry. In his statement, Trump emphasized the necessity of these tariffs to protect domestic manufacturers, saying, “In order to protect our Great Heavy Truck Manufacturers from unfair outside competition…” (Truck News). He framed the tariffs as vital for national security and the foundation of a strong economy, asserting, “Without them, we would face the opposite scenario.” (theguardian.com)

Chris Spear, President of the American Trucking Associations (ATA), voiced his concerns regarding the tariffs, emphasizing the potential economic strain on an industry already facing challenges. He stated, “At a time when the industry is just beginning to recover, these tariffs can decrease freight volumes and increase costs for motor carriers.” (trucking.org) Spear warned that fleet operators could see prices for new trucks increase by as much as $35,000 per vehicle, stressing the ramifications this would have on smaller carriers and overall freight movement. He further cautioned that prolonged tariff policies could lead the ATA to reconsider their strategies to mitigate adverse impacts on the industry.

The ATA also noted the broader implications of these tariffs on consumer goods transported by truck, warning that higher operational costs could ripple across markets, affecting a wide range of products, from food to electronics. Spear argued that while the administration’s focus on national security is important, it should not come at the expense of the freight industry’s recovery. (trucking.org)

In sum, as industry leaders like Spear assert the significance of national interests, they equally caution against measures that threaten the operational viability of the trucking sector during a critical recovery phase. The delicate balance between protectionism and economic sustainability remains a central theme in the discussion of these tariffs.

The reactions from industry stakeholders unveil a deep-seated anxiety regarding the newly imposed tariffs on heavy trucks. These insights pave the way for a clearer understanding of the impending challenges by demonstrating how the expressed concerns are not merely speculative but are rooted in forthcoming realities that the industry will face.

Industry leaders have laid bare their apprehensions, highlighting that the trajectory of financial impacts is not just a scenario to anticipate—it is unfolding in real-time. The facts that follow underscore the stark realities they cite: an increase in the tariff rate from 0% to 25%, effective October 1, 2025, threatens to inflate the prices of heavy trucks significantly.

Therefore, it becomes imperative to acknowledge these critical facts:

Outbound Links for Credibility

To enhance the credibility of the article regarding the economic implications of the 25% tariffs on heavy trucks, outbound links to authoritative sources have been added throughout sections 8 (Industry Leader Quotes) and 5 (Economic Impact Analysis).

Section 5: Economic Impact Analysis

The economic repercussions of the tariffs have been analyzed by various industry experts:

- Increased Manufacturing Costs: The American Trucking Associations estimates that the tariffs could significantly increase the cost of a new truck. For instance, up to $35,000 could be added to the price of a new Class 8 tractor due to these tariffs. More details can be found in the ATA’s statement on their official website.

- Projected Economic Losses: According to the Center for Automotive Research, U.S. automakers could face losses upwards of $108 billion due to the tariffs. This figure highlights the substantial financial impact on domestic industries tied to truck manufacturing. Additional analysis is offered by Perryman Group, which discusses broader economic implications.

- Freight Volume Reductions: The tariffs have seen major shifts in freight volumes, with reports showing reductions in shipping traffic at key ports. The U.S. Chamber of Commerce attributes this to the increased operational costs.

Section 8: Industry Leader Quotes

Industry leaders have spoken about the tariffs and their expected effects:

- Chris Spear, President of the American Trucking Associations, expressed concerns about the implications of the tariffs during their latest conference. His remarks can be examined further in their official statements.

- Volvo Group’s Outlook: The Volvo Group has outlined its position on the tariffs and their impact on the heavy truck market, calling attention to potential job cuts and declines in sales. Their latest findings can be explored here.

- Economic Analysts: Insights from economic analysts such as Arthur Laffer regarding the long-term consequences of the tariffs can be found on AP News.

These references provide readers with direct access to reputable sources that analyze and discuss the economic challenges posed by the 25% tariffs on heavy trucks. By doing so, the article enhances its credibility and informs readers effectively about the implications of the tariffs on the trucking industry.